Inclusive banking is desirable, but by forcing it on financial institutions, we could be making it tough for banks

A major issue confronting our financial system is the quality of assets. This has been exacerbated by the economic downturn, which is typically when loans stop performing. While restructuring is a way out for some cases, it poses conundrums for the lending institution as well as the regulator. An issue that comes up here is asset quality and priority sector lending. So far, with all the talk of inclusive growth, there are fixed norms for lending to vulnerable sectors. But, if one looks beyond the conventional commercial banking system, this problem is even scarier.

Within commercial banks, a little less than half of the non-performing assets (NPAs) originate in the priority sector (whose share in total credit is around 31-33%), and given that this sector is held sacrosanct, seldom do bankers raise objections and instead defend the concept as being necessary. In FY12, 4.4% of outstanding priority sector advances were classified as non-performing, while the same for non-priority sector was 2.4%. Further, growth in these NPAs was much higher than that in loans to this sector. Clearly, there are problems associated with such finance.

Within commercial banks, a little less than half of the non-performing assets (NPAs) originate in the priority sector (whose share in total credit is around 31-33%), and given that this sector is held sacrosanct, seldom do bankers raise objections and instead defend the concept as being necessary. In FY12, 4.4% of outstanding priority sector advances were classified as non-performing, while the same for non-priority sector was 2.4%. Further, growth in these NPAs was much higher than that in loans to this sector. Clearly, there are problems associated with such finance.

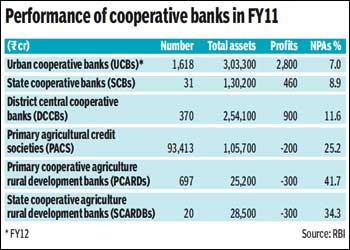

The accompanying table provides the picture of NPAs for various cooperative banks that are seldom analysed, which provide support to the rural economy and the small & medium enterprise (SME) segment.

The table shows that we have a large network of cooperative banks in the urban and rural spaces that offer various credit facilities to agriculture and SMEs. These banks have assets equivalent to around 12-15% of the commercial banking system, which is quite significant given that they address sections that would not qualify with commercial banks. Further, while the urban cooperative banks are profitable, the same does not hold at the rural level.

The significant aspect is the high levels of NPAs, which, at the level of rural development banks, is quite disastrous. Clearly, the business model does not work well at this level. The recovery ratios are also quite low and vary between 39.4% for PACs to 91.8% for SCBs. Given that these loans are directed mainly to farm-based borrowers, the problem is actually with the sector rather than the banks.

Two questions may be posed here. The first is whether the concept of priority sector lending is anachronistic in a regime where banks are answerable to their shareholders and adhere to prudential norms relating to bad assets and capital. Forcing banks to lend in areas where the probability of assets turning bad is higher may not be right. One reason why foreign banks do better is that they have less exposure to this segment.

The second relates to reforms in cooperative banking. Having NPA levels of 41.7% for PACs, 34.3% for SCARDBs, and 11.6% for DCCBs is definitely not viable. While there is a committee that has spoken about revamping them and providing more capital, the question to be answered is whether or not there are ways in which such lending is addressed. At the level of cooperative banks, the skill sets for evaluation of loans may be missing. But for commercial banks it is more the compulsion than the absence of skill sets that engenders such quality of assets.

Four solutions could be looked at, which should probably progress simultaneously. If banking has to be profitable and viable at the same time, the concept of priority sector should not be forced on banks and this level has to be brought down. In fact, it was suggested by the Narasimham Committee also a long time ago when financial reforms were invoked.

Second, the government should create a fund to compensate banks for such loans that are vulnerable to the vagaries of nature and tend to get magnified when there is a drought. This is a challenge given the fiscal constraints that already exist, but diverting a part of the MGNREGA expense for this purpose could be an idea as this will qualify as development expenditure. To lower this burden, various state governments could be asked to chip in.

Third, the government could impose an NPA cess on all borrowings so that a fund is created automatically by any bank on its loans, which can be used to make provisions or write-offs for NPAs. This will push up the cost of funds for borrowers, but in a way they would be made to subsidise the vulnerable sections. An extension could be to have a cess on all tax collections, which can also help. Interest earned for banks in FY12 was around R6.5 lakh crore. Assuming 70% from advances of which two-thirds from non-priority sector, interest would be around R3 lakh crore. A 1% cess on this would yield R3,000 crore.

The other solution is to allow credit default swaps on loans, which is not allowed today. The advantage here is that the risk involved in this lending can be mitigated by a third party. The issue, of course, will be that the CDS price will be high for farm loans that carry greater risk than, say, one to an SME. But, if bank loans are brought under this fold, it will help them to cover their risk theoretically at least. Mutual funds, foreign banks, NBFCs, insurance companies (which already are in the business of providing crop insurance and weather insurance to farmers) could be possible sellers of protection.

Inclusive banking is certainly desirable, but by forcing it on financial institutions, we could be making it tough for banks, especially when they are more susceptible to turning into NPAs. So far, we have skirted the issue as it sounded politically correct. But with the incidence of such lending turning unsatisfactory, alternative routes have to be explored or else we will get caught in a contradictory world where the best practices of BIS have to mingle with the pro-nationalisation thought process of the 1970s and 1980s, which looks irreconcilable as of now.

The author is chief economist, CARE Ratings. Views are personal