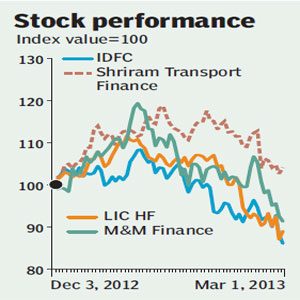

The Reserve Bank of India has released its final guidelines for new banking licences. These are different and, in many ways, tougher than the draft guidelines issued earlier. The final guidelines are most negative for standalone non-banking finance companies (NBFCs) or NBFCs belonging to a pure financial group that are not part of a corporate group, such as IDFC, Shriram or LIC Housing. Earlier, these were perceived to be the most eligible candidates for new banking licences. RBI has clarified that only widely held non-financial services companies/entities can sponsor an NOFHC (non-operative financial holding company), which, in turn, will float a bank.

The above NBFCs do not have any widely held non-financial company in the group that can float an NOFHC. The new guidelines are also negative for NBFCs belonging to business groups (MMFS?M&M Financial Services). RBI has made it clear that the financial entities under the NOFHC cannot undertake the business that RBI has permitted banks to do. This means that M&M Finance and others will all have to convert/transfer their businesses to the new bank, should their promoters decide to opt for a banking licence.

The above NBFCs do not have any widely held non-financial company in the group that can float an NOFHC. The new guidelines are also negative for NBFCs belonging to business groups (MMFS?M&M Financial Services). RBI has made it clear that the financial entities under the NOFHC cannot undertake the business that RBI has permitted banks to do. This means that M&M Finance and others will all have to convert/transfer their businesses to the new bank, should their promoters decide to opt for a banking licence.

The structure that these NBFCs were anticipating is that the NBFCs and the new bank would co-exist in the group, which can no longer happen. According to the current guidelines, L&T Finance, Bajaj Finance and Aditya Birla Nuvo (ABNL) are the most eligible candidates for new licences. RBI has clarified that licences will be given on a very selective basis. We do not expect the RBI to issue more than five licences. We believe the probability of a public sector entity obtaining a banking licence is low.

New guidelines

NOFHC will float a bank: Promoters interested in banking licences have to float an NOFHC. This NOFHC will have to be registered with RBI as an NBFC. The registered NOFHC can apply for a banking licence. It will house the bank and all other financial businesses/subsidiaries of the group Newly defined capital structure comes as a surprise: The RBI has come up with a detailed capital structure for NOFHC, which was not mentioned in earlier drafts. There are two important elements of the capital structure:

The promoter group (individual promoter and his relatives) can own only 10% of the NOFHC. A company promoted by the promoter group that is publicly listed, with more than 51% public shareholding, will have to hold at least 51% of the NOFHC. Therefore, for instance, L&T can sponsor an NOFHC, which can apply for a banking licence. Only non-financial services companies/entities and a non-operative financial holding company in the group and individuals belonging to the promoter group will be allowed to hold shares in the NOFHC. Financial services entities whose shares are held by the NOFHC cannot be shareholders of the NOFHC.

This new guideline is negative for standalone NBFCs/NBFCS belonging to a pure financial group that are not part of a corporate group, like IDFC, Shriram and LIC Housing.

Capital requirements unchanged: Capital requirement for a new bank is unchanged at R5 bn. The NOFHC will have to dilute its stake to 40% within three years (from the draft norm of two years) to 20% in 10 years and 15% within 12 years. The bank shall get its shares listed on the stock exchanges within three years of its commencement of business. The draft had set the listing requirement at two years. The bank should have a minimum CAR (capital adequacy ratio) of 13%, an increase from the 12% stated in the draft guidelines.

Existing lending NBFCs will have to be merged: The promoters/promoter groups with an existing NBFC, if considered eligible for a bank licence, will have three options:

(i) Promote a bank, if some or all the activities undertaken by the NBFC are not permitted to be undertaken by banks departmentally. In such cases, the activities undertaken by the NBFC that banks are allowed to undertake departmentally, will have to be transferred to the new bank, or

(ii) Convert the NBFC into a bank, if all the activities undertaken by it are allowed to be undertaken by a bank departmentally. In such a case, the NBFC shall have a minimum net worth of R 5 bn, or

(iii) Convert the NBFC into a bank and divest the activities that banks are not allowed to undertake departmentally. In such a case, the bank shall have a minimum net worth of R 5 bn.

The above guideline will be negative for the Shriram group and M&M Finance. These groups were hoping for a structure where the bank and NBFC could co-exist, which is not possible under the new guidelines. Converting to a bank will provide these NBFCs the benefit of retail funding, but it will also hurt their margins.

Foreign shareholding capped at 49%: Notwithstanding the current FDI policy, where foreign shareholding in private sector banks is allowed up to a ceiling of 74% of the paid-up voting equity capital, the aggregate non-resident shareholding from FDI, NRIs and FIIs in the new private sector banks shall not exceed 49% of the paid-up voting equity capital for the first five years from the date of licensing of the bank.

?Fit and proper? criteria: Entities/groups should have a past record of sound credentials and integrity, be financially sound, and with a successful track record of 10 years. For this purpose, RBI may seek feedback from other regulators and enforcement and investigative agencies.

Standard Chartered