Both HDFC and HDFC Bank trade at attractive multiples after the recent selloff in India. Markets will affect their near-term stock performance, but they are well-placed to do well. Balance sheets are strong and EPS (earnings per share) growth is likely to stay strong. We view this selloff as a great opportunity.

The recent selloff in Indian banks has affected good as well as weak banks: Viewed broadly, the selloff for the group is justified given corporate loans and the state of these corporate balance sheets. Investors don?t trust book values?and rightly so, in our view, given the amount of ?extend and pretend? taking place on bad loans. However, not every bank is equally exposed.

The balance sheets of HDFC and HDFC Bank are extremely strong: Unlike most of the other Indian banks, loan quality for these two is impeccable. Moreover, capital ratios are best in class, and profitability is very high and improving. Hence, the indiscriminate selloff has created an opportunity to own good businesses at fairly attractive multiples. The stocks could get cheaper, but we would own them from a longer-term perspective.

A legitimate concern is slowing growth: Till now retail loans have held up very well on growth and asset quality. The concern is whether they show weakness. We expect asset quality to remain strong, given low trailing growth for the system. However, growth will likely slow for the system. But given the state of competitors? balance sheets, we expect these two to gain share.

High teens/20% loan growth, plus strong asset quality should help EPS growth: We expect FY13?FY15 CAGRs (compound annual growth rate) of 17% for HDFC and 24% for HDFC Bank. It?s tough to find lenders with similar growth profiles and low risk to book. For HDFC, the subsidiaries are also doing very well (now ~30% of consolidated profits). Risks are a large-scale increase in unemployment and a sharp decline in property prices in India.

Investment case: In a weak market, the good get sold down with the weak?the absolute performance of HDFC and HDFC Bank over the last 12 months epitomises this. Both are doing very well in their respective businesses and have extremely strong balance sheets, yet their 12-month absolute performance has been weak. This has come against the backdrop of continued earnings compounding?as a result, their P/E (price-to-earnings) multiples are almost one standard deviation below their long-term (five-year) averages. They are not carrying any risks associated with the ongoing bust in corporate and infrastructure lending?implying that structural profitability is not at risk. The stocks could come under further pressure if the Indian market sells off, but, given where valuations are, we advocate building positions in them.

Balance sheets are very strong: The key concerns about lenders? balance sheets in India are:

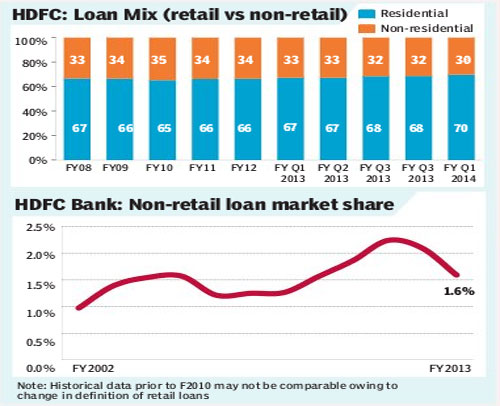

*Exposure to infrastructure and high impaired loans?For HDFC Bank, exposure to infrastructure is extremely low (for HDFC it doesn?t apply).

*Impaired loans ratio?The impaired loan ratios at HDFC and HDFC Bank are low with almost no restructurings. There has been no pushing the problems down the road, in our view. Moreover, coverage on existing bad loans is very high.

FY13-FY15 EPS growth likely to be 17% CAGR for HDFC and 24% for HDFC Bank: The ongoing slowdown in India will clearly affect volume growth in both mortgages and other parts of retail lending over the next two years for the industry as a whole. HDFC and HDFC Bank will also see some slowdown, but this will be protected through market share gain, in our view. One of the questions we often get from investors is that competitive intensity in retail is increasing?shouldn?t this hurt HDFC and HDFC Bank? We agree that every bank in India has been talking of retail lending as the only strategy, but market share trends show that leaders are increasing share. The reasoning is simple.

(i) With a base rate mechanism in place, it?s difficult for banks to compete on price.

(ii) While other banks are talking about focusing on retail, the bulk of management time is being spent on protecting asset quality issues, implying that they are unable to compete with HDFC and HDFC Bank.

(iii) Retail lending in India has been very slow over last four-five years, implying low risk for the industry. The penetration level in retail in India is very low compared to the rest of Asia.

HDFC Bank also has the option of corporate loan book growth in the non-risky areas. It?s currently punching well below its weight in non-retail lending?market share of <2%. With SOE (state-owned enterprise) banks fast becoming incapable of growing, HDFC Bank (and other private banks) can start taking market share in this book. HDFC too should be able to generate loan book growth in the high teens. The system loan growth in mortgages has been low over the last five years, and hence penetration levels are fairly low. The risk is a sharp correction in property prices across India. Moreover, HDFC has reduced the proportion of non-retail loans in its overall book over the last year. It can increase this book marginally, if enough demand from good borrowers exists. We are building in some slowdown in HDFC and HDFC Bank?s volume growth over the next two to three years. But in spite of that, the banks should deliver reasonably strong EPS growth.

Profitability at HDFC, HDFC Bank remains strong: HDFC?s ROE has been above 20% for most of last ten years; HDFC Bank?s ROE had been in the mid-to high teens over the last ten years. Over the last three years, profitability at HDFC Bank has improved. Retained earnings as a percentage of capital consumption per year are 90%. This used to be around 50% in the last decade. This implies that the pace of capital consumption at HDFC Bank has slowed, thereby pushing up RoE. The bank crossed 20% RoE in FY13.