We upgrade NTPC to Buy (from Add previously) with a target price of Rs 160 as the CMP (current market price) ignores the inherent strengths of the company relative to peers? (i) disproportionate allocation of coal due to proximity to coal mines, (ii) higher off-take due to low-cost take or pay arrangements, and (iii) consistent earnings growth with continued investment in new projects. At 1.1x P/B (price-to-book ratio), NTPC trades at a 45% discount to historical trading multiples, ignoring the inherent strengths of the company.

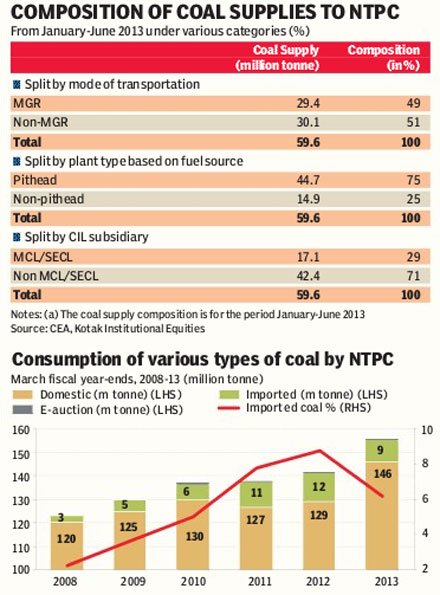

Proximity to coal mines will ensure higher coal allocation compared to peers: Proximity to coal mines, dedicated evacuation infrastructure and supplement through captive coal blocks will likely allow NTPC to continue to enjoy a disproportionate allocation of domestic coal supplies. A bulk of NTPC?s extant power plants receives coal supplies through dedicated MGR (merry-go-round rail) facilities, with 75% of coal supplies from pit-head locations. Only two coal sources (MCL-Talcher and SECL-Korba) are not fully meeting coal supply commitments currently. Even for incremental capacities, nearly 30% are dependent on captive coal.

Low cost of generation will keep it ahead of peers on cost curve: With low-cost domestic coal continuing to dominate fuel sourcing and a relatively ageing fleet (with a mix of new and old plants), average cost of generation for NTPC will continue to be superior to that of IPPs (independent power producers)?NTPC had an average fuel cost of 1.7/kwh in FY13 compared to >2.5/kwh for private sector players. While cost of generation is less ominous for NTPC (under cost-plus regime), efficient players such as NTPC will continue to enjoy a higher off-take as state distribution utilities become more cost conscious.

NTPC trades at deep discount to historical multiples: At 1.1 P/B and 9x P/E (price-to-earnings ratio), NTPC is trading at historical lows, while ignoring the inherent strength of the cost-plus business model as well as the 9% CAGR (compound annual growth rate) in earnings factored by us (over FY2011-16e). We upgrade NTPC to Buy with a revised target price of Rs 160 (165 previously). While fuel security remains an area of concern, cost-plus sale arrangement makes NTPC relatively better-positioned in comparison to IPPs with lower fuel and off-take risk even as availability-based incentive ensures resilience of earnings.

In our view, improved visibility on the capacity addition programme beyond the immediate 14 GW targets as well as clarity on sustenance of returns despite coal availability issues with a pending regulatory review will provide long-term earnings visibility.

Continued investment in projects will enable consistent earnings growth: With 20 GW of capacities under construction and capex meeting targets (197 bn against target of 209 bn), the growth prospects for NTPC remain on track. The earnings profile of NTPC is in sharp contrast to private players who enjoyed high double-digit growth on the back of low capacity base, but will stagnate over the next few years as incremental investments in power plants have nearly come to a standstill.

NTPC also has a portfolio of 35 GW of under-development projects, which could ensure a more distributed capacity addition for FY17 and beyond. We expect a majority (80-90%) of these capacities to be commercialised only in the next Plan period.

We note that a large part of the project pipeline is back-ended for commissioning by FY16e and beyond, as only 2 GW of capacities are expected to be commissioned in FY14 and FY15. (The larger projects?Bark (3,300 MY), Lard (4,000 MY) and Maude Stage II (1,320 MY) are likely to be commissioned only in FY2016-17.

Regulatory review may throw in lesser surprises: While the CERC (Central Electricity Regulatory Commission) approach paper for tariff regulations for 2014-19 is still at a preliminary stage, we believe the review will address key issues hindering the progress of the sector?while maintaining a balanced approach between return profile for the utilities and tariffs for the consumers.

The draft paper aims to tighten norms for capital cost reimbursement by prescribing timelines for standard construction period and increasing the useful life of the assets to reflect a more realistic picture, while taking a more constructive view on operational costs by proposing more lax availability factors, taking into consideration short-supply of coal and indexing maintenance costs to inflation indices.

?Kotak Institutional Equities