Earnings momentum should continue to strengthen with steady domestic growth and gradual margin recovery in international T&D (transmission & distribution). Consolidated EPS CAGR (earnings per share, compound annual growth rate) of 41% (F13-15e; low base) has upside risk from faster rise in international margins or faster revenue growth in better macro conditions.

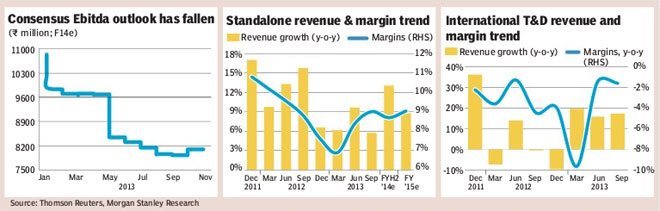

The revenue trend remains muted, but margin gains from recent lows (210bps gains in last two quarters)?which we view as sustainable?should drive earnings growth.

Challenges in international T&D business: Revenue growth (aided by currency) has held up (order book too grew 11%), but margin gains were lower than we had estimated. Margins should improve gradually in ensuing quarters with restructuring gains and execution.

Slowing order inflow poses revenue risk: Order intake fell 13% to R22 bn; order book grew a modest 4%. The management argues that the focus is on high margin orders, but if flows remain muted, F15e (estimates) revenues could moderate: we expect 9% in F15 vs. 11% in F14.

We raise our PT (price target) by 2% to R130 (22% upside): This reflects (i) modest cuts to EPS estimates for the standalone business (valued on P/E), (ii) rolling valuation forward for the standalone business and (iii) the bulk of the EPS estimate cut is in the international business (valued on PB?price-to-book– because it is loss-making), hence the impact on target is modest. Our scenario weights are unchanged.

Key risks: Weak international earnings/disappointment in domestic EPS lead to market multiple contraction.

Maintain our Overweight rating: We believe our thesis of gradual recovery in the domestic business (partly aided by a low base) is playing out, notwithstanding a tough macro environment. Recovery in the international T&D business has not been along expected lines. However, with the company breaking even at the Ebitda level at most international operations (except the US and Canada), we expect continual improvement in margins over the next few quarters.

We understand that revenue momentum could moderate given slowing order book growth (in line with the macro environment), but margin gains in both the domestic and international operations should drive earnings growth.

Crompton?s stock has posted an absolute gain of 14% and outperformed the broader market (Sensex) by 11% in the last six months, notwithstanding the decrease in consensus earnings outlook.

Investors are focusing on earnings recovery led by operational efficiency over the next few quarters, and we believe this has led to expansion in the stock multiple. In our view, the international T&D business will deliver gradual margin pick up over the next few quarters and domestic business will benefit from low base and management?s focus on margins in the new orders, which would drive recovery in earnings momentum. We have cut our consolidated earnings estimates by 46% for F14 and 38% for F15, but that still implies 36% and 43% core earnings growth in F14e and F15e, partly from a low base. Our standalone earnings estimates are down a modest 3% and 7%. The cuts to our consolidated and standalone EPS estimates also reflect a reduction in share count following the company?s recent share buyback. Our revised target of R130 (from R128), implies 22% upside.

While consolidated earnings are important, in our view, in the near term the focus is likely to be relatively higher on standalone earnings. Given capital goods companies are reporting weak earnings, if Crompton?s standalone business continues to do well (from low base), this should support stock performance. On consolidated earnings, visibility is low and hence we believe the Street should be fine as long as margins improve directionally.