Focus on containing impairment levels over growth: Our recent interaction with the management highlighted that the business environment?loan impairment and growth?remains challenging in the corporate portfolio. At this stage, there is a greater focus on loan impairment as compared to growth. We maintain our Reduce rating with TP (target price) at R610 (from R550 earlier) as RoEs (returns on equity) are subdued (13%), while earnings growth of >40% in FY15e is primarily driven by better treasury contribution. Earnings (adjusted for treasury income) are likely to grow <10% CAGR (compound annual growth rate) in FY15-16e.

Takeaways: The following were the key takeaways from our discussions with the management: (i) Corporate loan demand remains subdued and the bank has been cautious on taking incremental exposure in this portfolio; (ii) pressure on NIM (net interest margin) will continue as the bank is shifting focus towards low-risk assets; (iii) considerable progress to maintain loan impairment ratios at current levels while any improvement would require better economic growth trends, which is subdued currently; (iv) impact of the change in annuity tables yet to be ascertained but could get crystallised by Q4FY14e (estimates); and (v) no near-term requirement to dilute capital as tier-1 ratio is at 9%.

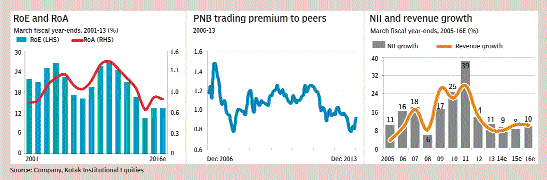

Earnings driven by better contribution from treasury: We believe Punjab National Bank could deliver a strong earnings growth in FY15e of >40% year-on-year, primarily on the back of strong contribution from treasury income (net treasury income in FY14e was at -9%, which is likely to increase to 17% of PBT?profit before tax– in FY15e). However, earnings growth, adjusted for treasury contribution, is likely to remain subdued at <10% CAGR for FY2015-16e. NII growth is likely to remain subdued (<10%) as loan mix is shifting towards low-risk lending.

Wait for firm trends of improvement: We maintain our Reduce rating and value the bank at R610 (rolling 12-month basis from R550 earlier). At our target price, the bank would trade at 0.7x (times) book and 5e EPS (earnings per share). RoEs at 10-13% would be closer to a decade low. The bank is currently trading at 15% long-term valuation discount to its public sector peers and closer to the bottom on a ten-year basis.

Our rating is driven by (i) lack of clear trends on impairment ratios as the risk for further slippages, especially from the restructured portfolio, is high, (ii) scope for RoE improvement is constrained by high credit costs. Any improvement in loan impairment may not immediately result in RoE expansion as the bank would look to improve coverage ratios from current levels, and (iii) the extent of impact of the revenue slowdown due to the correction in balance sheet towards low-risk lending has still not been ascertained. Meeting management guidance on NIM of 3.25% would imply negligible earnings growth for about a year.

Select segments could show better trends: Broad trends from the previous quarter and discussions with the management indicate that the focus is primarily on containment of loan impairment ratios. Q2FY14 saw gross NPLs (non-performing loans) at 5% and restructured loans at 11%. A large share of the restructured loan portfolio were from (i) infrastructure, primarily from power sector post the SEB (state electricity board) reforms, and (ii) iron and steel. In the infrastructure portfolio, the bank has restructured 35% of its overall portfolio, one of the highest among peers.

NIM has scope for moderation: PNB has guided that there is scope for further moderation in earnings in the medium term and the bank would target 3.25% levels from current levels of 3.5%. However, the reduction may not be immediate. We believe that the impact is led by a few factors? (i) focus is shifting to retail and other low-yielding segments as compared to large corporate lending, (ii) risk appetite to underwrite corporate lending could have significantly diminished, resulting in pursuit of low-yielding loans in the corporate portfolio, and (iii) significant NPL has resulted in significant de-recognition of interest income and pressure continues.

However, we do note significant progress on the liability side of the balance sheet:

(i) CASA (current account savings account) has moved back to 41% (domestic deposits), which includes a healthy growth of 13% in savings deposits. The management indicated that it has been able to arrest the decline in market share of savings account mobilisation to private banks as there has been increased focus from the field officers. We would not be able to ascertain this change in trend immediately as RBI?s data comes with a lag of a year, and (ii) slow growth in loans has resulted in reduced dependence on wholesale liabilities. As of Q2FY14, the overall wholesale liabilities were at 6% as compared to >20% in Q2FY13.