Retain reduce with TP of Rs 770, 30% downside: The reported same store sales growth (SSSG) of -2.6% for Q3FY14 is significantly below our estimate. H1FY14 saw SSSG of 6.5%, which means underlying consumer demand has become considerably worse over the past quarter. Check: Jubilant Foodworks Ltd shares

The management attributed the decline to weak economic growth and said they are optimistic about a recovery in the medium term. However, the near-term outlook remains uncertain and, in our view, SSSG trends are likely to remain muted over the next two-three quarters.

Any recovery in H2FY15 is built more on hope at this stage, and we see more cuts to consensus earnings coming in the next couple of quarters. Margins also disappointed during the quarter (down 260 bps y-o-y) with Dunkin Donuts business continuing to be a drag. Our earnings and TP (target price) are cut to factor in a slower growth environment, and with the stock trading at 35.6x FY16F (forecast) earnings, vs a sector average of 23x, we retain our Reduce rating.

Catalysts?a sharp recovery in SSSG and an improvement in margins: The company?s business model is built on the underlying assumption that SSSG will be strong, which helped drive both growth and profitability. We believe in the near term, SSSG recovery is unlikely to come through, hence valuations should see a correction down to nearer the consumer average.

Valuation: JUBI trades at 35.6x FY16F vs. sector average of 23x JUBI trades at 35.6x FY16F vs a sector average of 23x. Valuations remain expensive despite the fact that the earnings profile is sharply lower vs FY11-12, when SSSG was very strong. Current valuations build in strong SSSG over the next couple of years, which we believe is unlikely given the slowing momentum in demand.

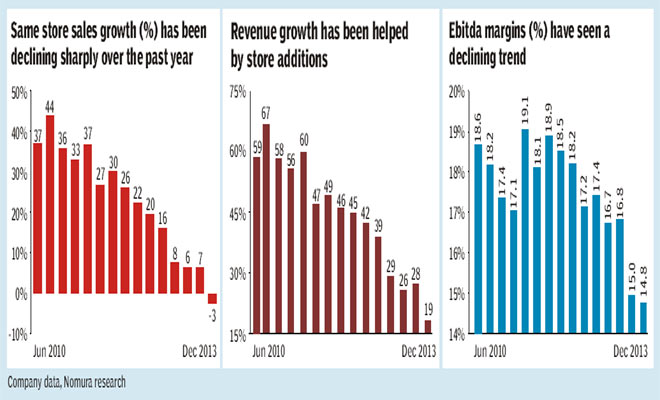

Q3FY14 results significantly below expectations: While sales were 8.8% below our estimate, PAT was 20.9% below our estimate and 17.4% below the Street. For the first time since 2009, SSSG has turned negative. This is reflective of the sharp decline in new customer acquisition as well as weak underlying consumer demand. While there was expectation that a turnaround in growth was still far away, investor expectation after the first couple of quarters was for mid single-digit SSSG to continue. In that context, the Q3FY14 results were a significant disappointment, with underlying demand trends getting significantly worse on a sequential basis.

Key numbers

Net revenues increased 18.5% to Rs 4.6 bn against our expectation of Rs 5 bn and Street expectations of Rs 4.9 bn.

SSSG for the quarter at -2.6% was below our estimate of 7%.

Ebitda came in at Rs 674m, vs our estimate of Rs 792m and consensus at Rs 758m.

Ebitda margin came in at 14.8%, down 260bps y-o-y. We were expecting Ebitda margin at 15.8% (down 160 bps y-o-y) and the street was at 15.4% (down 200 bps y-o-y).

The key negative surprises were gross margin, which declined 100 bps y-o-y, and rental costs, which rose 90 bps y-o-y.

PAT came in at Rs 336m against our expectation of Rs 425m and consensus at Rs 407m.

Near-term outlook remains uncertain: On the conference call post-Q3 results, the management highlighted that a significant part of the declining SSSG is on account of the weak macro environment with consumer demand being low. We believe the near-term outlook for consumer demand remains uncertain, hence a recovery will not come through over the next two quarters at least. However, the company continues to guide strongly for store additions, which will continue to impact margins in the near term. We believe the SSSG trend may remain at flat to down over the next two quarters, which will act as a negative catalyst for the stock.