Biggest impediment to a roaring bull market is the state of domestic liquidity

The year 2012 was about defensive and quality stocks. We think this is changing ? 2013 may look different. As usual, change is permanent even though changes are not. The earnings cycle is likely to inflect positively, setting the stage for: (i) higher equity prices; (ii) growth to beat quality; (iii) cyclicals outpacing defensives; and (iv) stock picking yielding to sector approach in equity portfolios.

Most of 2012 was about global factors: This was best evidenced by the all-time high that correlation of returns between Indian and global equities hit. Through the year, market participants argued for lower share prices premised on India?s poor macro backdrop. India?s high external deficit hinged it to global outcomes, making global rather than local factors the primary driver of equity returns. QE has stemmed India?s tail risks from its macro imbalances and coupled with a bit of domestic policy progress, return correlations have begun to decline, albeit from a historical high.

Most of 2012 was about global factors: This was best evidenced by the all-time high that correlation of returns between Indian and global equities hit. Through the year, market participants argued for lower share prices premised on India?s poor macro backdrop. India?s high external deficit hinged it to global outcomes, making global rather than local factors the primary driver of equity returns. QE has stemmed India?s tail risks from its macro imbalances and coupled with a bit of domestic policy progress, return correlations have begun to decline, albeit from a historical high.

For 2013, we see the following:

* A new earnings cycle?A steady recovery in broad market earnings growth to 20% by end-FY2014.

* 26% Sensex upside?largely from earnings progression, not multiple expansion.

* An upcycle in earnings, strong global liquidity and supportive valuations are helping the market. Domestic liquidity and flattish yield curve are still impediments.

* Preferred portfolio strategy: Growth over quality (high free cash flow, high return on equity, low capex), cyclicals over defensives, active sector positions vs. stock selection.

Key assumptions: No major risk-off in the world, small domestic policy tailwind, elections not before year end, range-bound crude oil and front-ended rate cuts.

2013 Outlook

Our probability-weighted outcome for the BSE Sensex is 23,069 for December 2013, implying 26% upside.

Base case (60% probability): Sensex: 23,097. Fiscal prudence, steady improvement in infrastructure spending and progress on GST (goods and services tax), no major global risk-off with range-bound crude oil prices, reasonable capital flows and steady monetary easing on the back of slight moderation in inflation. Slower global growth will be beneficial for corporate margins in India as well as inflation. Sensex earnings growth at 10% and 19% for FY13 and FY14, respectively.

Base case (60% probability): Sensex: 23,097. Fiscal prudence, steady improvement in infrastructure spending and progress on GST (goods and services tax), no major global risk-off with range-bound crude oil prices, reasonable capital flows and steady monetary easing on the back of slight moderation in inflation. Slower global growth will be beneficial for corporate margins in India as well as inflation. Sensex earnings growth at 10% and 19% for FY13 and FY14, respectively.

Bull case (20% probability): Sensex: 28,137. Global calm and a measured recovery in global growth, strong policy action, range-bound crude oil prices and rate cuts in response to a fall in inflation in Q1FY13. Sensex earnings growth rises to 15% and 22% in FY13 and FY14, respectively.

Bear case (20% probability): BSE Sensex: 17,918. Weak policy action, a fragile global situation culminating into some sort of crisis and/or supply shock in crude oil prices causing continuing tightness in monetary policy. Sensex earnings growth falls to -2% for FY2013 but rises 12% for FY2014.

Forecasts for 2013: Sensex likely to hit new high

We think that earnings growth is likely to improve over the next 4-6 quarters, and therefore, the earnings revisions breadth will also rise. However, the recovery in earnings is likely to be at a steady pace unless there is a major positive change in the investment rate or the current account. Our Sensex forecast is for 26% upside. For a full-blown bull market (our bull case), we need bullish steepening of the yield curve and significantly better domestic liquidity (in the form of lower short rates). Our bear case is anchored to global developments.

Earnings growth on a recovery path: Over the past four years, profits have grown significantly slower than nominal GDP due to compressing gross margins and rising rates. From a top-down perspective, corporate profits lost share in GDP?the same thing as saying that margins fell ? for two reasons. The fall in the investment rate relative to household savings (implying falling utilisation of capacity) and the rising current account deficit (implying loss of production to the world), offset partly by rising fiscal deficit or lower public savings were key explanatory factors. This macro mix largely reflected domestic policy choices which kept real rates negative, an unsupportive global growth environment, and the purging of the excesses from the previous cycle. Looked from another perspective, the fall in profit margins explains the bulk of the rise in India’s CAD (current account deficit) between FY08 and FY12.

What has changed? Revenue growth outlook is improving since M1 growth has seemingly put in a firm base at the end of last year and it leads revenue growth by about two quarters. The base effect is favourable for Ebitda (earnings before interest, taxes, depreciation and amortisation) margins. Gross margins have started to rise from decade lows (helped by slowing pace of commodity prices increase) and improving operating leverage will help margins. Interest rates could have peaked as the year-on-year fall in CP (commercial paper) rates suggest and interest costs are unlikely to rise at the same pace as seen recently. From a top-down angle, the shift in terms of trade could be the inflexion.

The key risks to our view on earnings include an increase in commodity prices, a serious global risk off with negative implications on India?s BoP (balance of payments) and interest rates and another leg down in the investment cycle. To be sure, our economist is forecasting neither a big investment cycle nor a fall in the CAD.

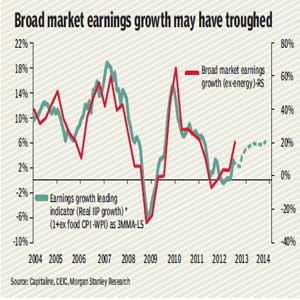

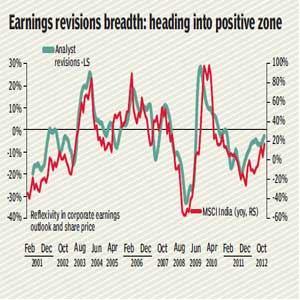

Our leading indicator for broad market earnings signals that growth could improve from an average of 1% over the past four quarters to about 10% in the coming three (see chart) and then to around 20% by the end of FY14. Corporate fundamentals have been relatively better in India than the rest of the world in 2012. An absolute upturn in earnings bodes well for the equity market overall as well as for the credit cycle. While the earnings revisions breadth has improved from the trough, its level as well the consensus earnings forecast shows lack of optimism on the earnings outlook (see chart).

Market likely to breach new high in 2013: Our framework suggests that there are four fundamental ingredients to a bull market: (i) Bullish steepening of the yield curve (as a leading sign of better growth); (ii) Expanding profit margins (to translate GDP growth into profit growth? higher share prices need profit growth); (iii) Attractive valuations; and (iv) Liquidity. At this moment, valuations are attractive and ready for a new bull market. Sentiment also visited a historical low at the end of 2011 and has improved since then. Profit growth is entering a period of recovery, but we do not believe a full-blown margin expansion cycle is on hand. The biggest impediment to a roaring bull market is the state of domestic liquidity. Short-term interest rates move around with liquidity. However, the liquidity that stock markets need varies with the level of share prices (i.e. valuations). Liquidity required to move stocks is higher when share prices or valuations are higher.

Key themes for FY13

The correlation of stocks with the Sensex is approaching lows warranting wider sector positions. Cyclicals look ultra cheap versus defensives. Small and mid-caps look very attractive. Hence, our portfolio strategy is:

(i) Raise sector positions: We have increased our active position to 1,100bp from 500bp in September.

(ii) Prefer cyclical sectors: Our pecking order is financials, consumer discretionary, industrials, energy & materials.

(iii) Focus on EPS (earnings per share) growth and a positive delta in ROE (return of equity) for stock selection while still avoiding high financial gearing and remaining sensitive to valuations.(iv) Large-cap cyclicals is the way forward, although some sprinkling of mid- and small-caps is recommended.

Cyclicals enjoy valuation comfort: The outperformance of defensives over cyclicals since the start of 2008 has taken the relative valuations of cyclicals to multi-year lows. There is little to distinguish between domestic and global cyclicals. History suggests a period is coming when cyclicals start outpacing defensives. If the past ten years’ history is anything to go by, the relative valuations of domestic cyclicals versus defensives indicate 56% relative outperformance for domestic cyclicals over the coming 12 months. Given our view that corporate earnings are likely to improve in the coming months, cyclicals will likely deliver better fundamentals. Thus, cyclicals enjoy better valuations and improving prospective fundamentals.

Macro approach warranted for portfolios: Our strategy between macro (big sector positions) and micro (stock focus) is determined by our correlation work. The average of the correlation of stock returns in the broad market with the Sensex returns tells us whether the market is being influenced by macro conditions or idiosyncrasy. When the correlations are high and rising (like in most of 2011 and 2012), it means the macro outlook has wielded undue influence on stocks. Our strategy is to do the opposite, because individual factors also drive stock returns. The opposite holds true as well. Hence, when correlations are low, macro influence is absent, and the market is overly focused on idiosyncratic stock factors?to us, this is the time to get macro. Correlation extremes represent a chance to be contrarian. Since their peak in January 2012, correlations have declined and are now at levels consistent with a bigger macro trade. Hence, investors need to get more macro in their portfolios. Valuation (P/B) dispersions could also be peaking, and mean reversion is likely?implying narrower valuation gaps between cyclicals and defensives.

Morgan Stanley Research