Good going. Reliance Industries

reported Q3FY14 net income at R55.1 bn, 6% ahead of our estimate led by (i) better-than-expected performance of the refining segment and (ii) higher other income.

The recent improvement in refining margins, higher gas price from April 2014 and progress in new core business projects augur well for stock performance. We retain our Buy rating on the RIL stock while revising our SOTP (sum-of-the-parts) based target price to Rs 1,030 (Rs 980 previously) by rolling forward to FY2015 estimates.

Refining segment and other income drive beat of net income: RIL reported net income at Rs 55.1 bn (+0.2% year-on-year and +0.4% quarter-on-quarter), 6% ahead of our estimate of Rs 52.1 bn led by (i) strong financial performance of the refining segment and (ii) higher-than-expected other income at Rs 23.1 bn (+12% q-o-q).

We are surprised by sequentially stable Ebit of the refining segment despite lower crude throughput and refining margins?this implies savings of $0.35/bbl (barrel) on operational costs. Reported Ebitda (earnings before interest, taxes, depreciation and amortisation) declined 9% y-o-y and 3% q-o-q to Rs 76.2 bn, 2% ahead of our expected Rs 74.6 bn. The y-o-y decline in Ebitda despite 13% depreciation in the rupee-dollar exchange rate reflects lower refining margins (-$2/bbl).

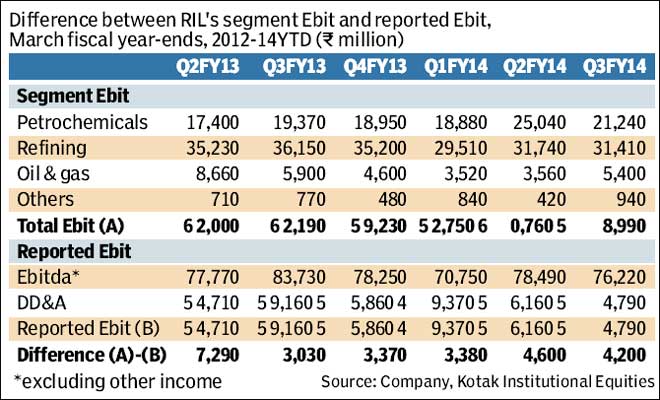

Q-o-q decline in petchem Ebit; improvement in E&P segment Ebit: RIL?s petchem segment Ebit declined by 15% q-o-q to Rs 21.2 bn (+10% y-o-y) led by (i) weaker margins for polyester and vinyl chains and (ii) presumably lower sales volumes. Refining segment Ebit declined 13% y-o-y to Rs 31.4 bn (-1% q-o-q) despite a weaker rupee exchange rate, reflecting lower refining margins and lower crude throughput (-0.5 mn tons y-o-y). E&P (exploration and production) segment Ebit increased to Rs 5.4 bn in Q3FY14 from Rs 3.6 bn in Q2FY14 led by higher sales volumes for oil and condensate as reflected in higher revenues (+18% q-o-q).

Financial highlights

Ebitda and net income: RIL?s Q3FY14 Ebitda declined by 9% y-o-y and 2.9% q-o-q to Rs 76.2 bn. The y-o-y decline in Ebitda reflects lower refining margin and lower crude throughput. However, net income remained stable at Rs 55.1 bn versus Rs 55 bn in Q3FY13 and Rs 54.9 bn in Q2FY14, reflecting lower depreciation and higher other income.

Higher other income: Other income increased by 33% y-o-y and 12% q-o-q to Rs 23 bn. However, RIL?s cash and cash equivalents decreased to Rs 887 bn at end-December 2013 versus Rs 905 bn at end-September 2013.

Lower interest expense: Interest expense declined to Rs 7.9 bn compared to R8 bn in Q2FY14 and Rs 8.1 bn in Q3FY13; gross interest expense, including interest capitalised of R1.9 bn, was R9.8 bn. RIL?s implied interest rate was 4.7% in Q3FY14 versus 4.8% in Q2FY14 and 4.9% in FY2013.

Lower DD&A charges. RIL?s reported DD&A (depletion, depreciation and amortisation) expense declined 12.8% y-o-y and 4% q-o-q to Rs 21.4 bn. RIL has not provided a break-up of depreciation and depletion separately.

Higher effective tax rate

y-o-y: Effective tax rate was 21.2% compared to 20.1% in Q2FY14 and 19.7% in Q3FY13. We remain surprised by the lower cash tax rate of 20.3% in 9MFY14 given (i) full taxation of income from petchem segment and the first Jamnagar refinery; other income will also be largely taxed at the corporate tax rate of 33.99% and (ii) the applicability of MAT (minimum alternate tax) rate of 20% on the income from SEZ refinery and E&P (exploration and production) segment.

Increase in net cash balance: RIL has reported net cash balance of Rs 74 bn at end-December 2013 against net cash balance of Rs 66 bn at end-September 2013. The modest increase in net cash balance despite Rs 77 bn of gross cash flow generation (net profit + DDA + deferred taxation) reflects capex in ongoing core business projects. We note that net addition to fixed assets was higher at Rs 276 bn in 9MFY14 led by forex-related capitalisation of Rs 75 bn.

Retain Buy: We retain our Buy rating on the stock with a fair value of Rs 1,030. We expect the company to benefit from (i) the recent improvement in complex refining margins, (ii) increase in domestic gas price effective from April 2014 and (iii) progress in new core business projects. However, we do see risks to fair value from potential large investments in the telecom segment, which may dilute earnings at the consolidated level in the medium term.