Tweak up estimates/PO on strong outlook in international business: Tata Consultancy Services profit after tax was 2% ahead of our estimate, on in-line revs (revenues) and margins, and slightly higher forex hedging related gains. International revs grew at a stronger than expected 3.8% sequentially in USD terms while India (6% of revs) declined higher than expected by almost 6% q-o-q.

CEO Chandra expects rev growth to accelerate in FY15, given an improving environment and TCSs strong competitive position. We forecast largely steady margins. We tweak up our estimates by 1-2% and raise PO (price objective) to Rs 2,650 (vs Rs 2,600) at a target CY15e PE (price-to-earnings multiple) of 20x, in line with its current one-year fwd PE and our forecast CY13-15e EPS CAGR (earnings per share, compound annual growth rate) of 21%.

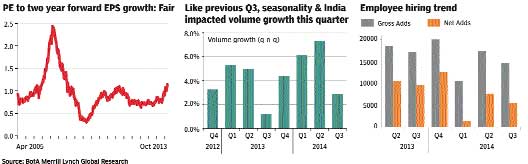

Revenue outlook continues to trend up

Bullish commentary on deal pipeline: Management commentary on the call suggested a strengthening deal pipeline for TCS going into next year driven by:

n Improving market presence for TCS in continental Europe

n Improving environment for discretionary IT spends like digital initiative and regulations related spends

n Continuing market opportunity around cost optimisation/ simplification of IT landscape.

In particular, it highlighted the emerging opportunity in the digital space (a collective term for opportunity relating to cloud, mobility, big data & analytics, social and artificial intelligence) that is likely to emerge as a key driver of incremental discretionary revenues. Per company, project sizes in this space have been gradually increasing over the past few quarters and are likely to remain on a secular growth curve over next few years.

We expect services spends around big data and mobility to be on cusp of entering a high growth phase. TCS appears best positioned amongst India-listed integrated vendors to benefit from this opportunity.

Company expects FY15 to be a year of higher growth than FY14 despite weakness in domestic market likely continuing until Jun/Sep due to elections in India.

Large deal win momentum on track: TCS won a healthy eight large deals this quarter. This is despite push out of decisions in certain deals in retail vertical from December to March quarter. We expect an improving outlook for Indian vendors in the large deals space driven by accelerating growth in continental Europe and Infrastructure services. TCS is well positioned to benefit from both these trends. Hence, we continue to expect a healthy momentum in large deal wins for the company.

Hiring outlook in-sync: Employee headcount for TCS expanded 2%, comparable to its volume growth. It has upped FY14 gross hiring target from 50k employees to 55k which implies 12k+ gross hires in Q4FY14. Campus offers for next year are likely to be 25k (flat y-o-y) given the focus on just-in-time hiring that is likely to include off-campus fresher hiring.

Industry leading margins: We believe TCS can broadly maintain its industry leading margins forecast at 29% for FY14 on a constant currency basis. Our margin comfort stems from scale benefits, focus on productivity, best-in-class employee retention (14% annualised last quarter vs. Infy?s 23%) and investments in IP/new markets likely paying off. For example, this quarter?s utilisation rate of 84.3% is at an all-time high for the company. This suggests a continuing focus by TCS on further tightening its delivery organisation.

Q3: Weakness in India masks strength in international revs: Growth was driven by continental Europe growing over 5% q-o-q and verticals of telecom, manufacturing and life sciences growing at a robust 6-8% q-o-q. US and the verticals of banking & retail grew at 2%, due to the impact of furloughs and seasonality. Constant currency realisation increased by +0.74% likely helped by mix. Margins declined 42bps q-o-q. Gains from utilisation and offshore shift in effort reinvested in the business. Industry low employee attrition at 13% qrt annualised vs 21% at Infy/29% at HCLT.

Rev growth to accelerate: We believe TCS is in a strong competitive position given its scale, experience and early investments in the digital space. It has upped the hiring target by 5,000 to 55,000 for FY14. While TCS Ebit margins are higher, we believe TCS is likely to maintain margins within a narrow band at 28-28.5% over FY15/16 given likely gradual pace of investments and relentless focus on productivity.