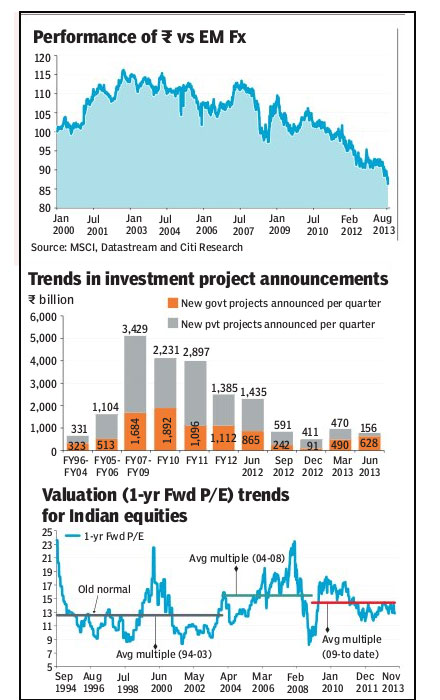

The new uncertainty: India’s one near-given was falling interest rates and inflation; with RBI?s currency defence, that has fallen. India is now swamped with uncertainty?monetary/currency policy, economic/investment revival, earnings, flows and elections. That is smashing the market currently, but more fundamentally it pushes out any economic/earnings/valuation-based revival. We lower our BSE Sensex target to 18,900 (from 20,800)?a 12.5x target multiple (95-03 averages); it’s the ‘old normal.’

SECTOR RATING

OVERWEIGHT

PHARMA; TELECOM; ENERGY; IT SERVICES

NEUTRAL

BANKS

UNDERWEIGHT

CONSUMER STAPLES: MATERIALS

Defences breached

The Indian rupee‘s defence hasn?t worked, but it has raised and inverted the yield curve (second time in ten years), eroded wealth/value (equities, now fixed income, waiting for property) and is stalling the funding market. It hurt the market (-11%$ rel. GEMs in 1m) and it might not be over yet, albeit such falls could offer some near-term bounces (rate/liquidity policy reversal, global support). Defences down, risks up.

FY14?s gone, it?s FY15 & beyond that is the challenge

This is the fundamental question?how hard has medium-term growth been hit? That?s because there is now a corporate confidence/credit crunch, likelihood of it spilling to the consumer, challenges on reform/regulatory issues, and tough markets are making it harder. It’s going to hurt?FY14?s gone, start thinking about FY15 and beyond.

Don?t write India off; it has fixed itself before

India has been here before, and fixed itself; on macro-currency (2002), fiscal deficit (2003-08) and inflation (2001-03). And bottom-up too?asset quality (1999-07), tech bubble (2002), retail credit (2009) and most recently telecom (2012). India needs a policy/bottom-up pullback, some luck and time, and don?t write it off. But currently, there?s little to write home about.

India has seen such market months before, and bounced back. But more important, it has been able to materially address macro-economic and business challenges, after it had been written off.

This holds true for at the macro-economic levels: be it its fiscal deficit, which it reduced from 6%+ to under 3% over the 2003-08 period; inflation?which it sustainably reduced to sub-5% in the 2001-03 period; and its currency, which appreciated almost 25% (R49 to sub-R40) over 2001-07. These no doubt were very strong growth years, boosted by global capital, but there was method and direction from the policy makers. Can this be done again? Hard to call, but there is government intent (an execution on fiscal consolidation in FY13, and some success on inflation), but it will need a supportive global and market environment, and a fair degree of patience.

This is even truer for the corporate sector, and we have more confidence in its ability to fix itself (from the current stretched position for some) with or without the government?s help. This was very much in evidence with the IT services, which regrouped very effectively after the 2000 technology/ Y2K bust, and came out much stronger. It?s the case with the recent consumer credit cycle in 2009:post-aggressive restructuring, it is among the stronger and safer growth businesses currently.

And of course, the telecom sector–an outcast until the last year, is now one of the few well-placed sectors in the market (even as governmental challenges have continued), and it is one of the primary OWs (overweight) in our model portfolio. We would keep an eye out for power, infrastructure, and real estate!

The old normal (FY95-03) and?patience

India seems set to go back to its ?old normal? (FY95-03): lower growth, higher uncertainty and yes, lower market multiples. That?s where we peg our market target; 12.5x 1 year forward earnings, or a Sensex target of 18,900 (+3%). In our model portfolio, we OW pharma, telecom, energy and IT services (up from Neutral); Neutral banks (downgraded from OW); and UW (underweight) consumer staples, materials. India?s ?new normal? from here is very likely to be its ?old normal?, which lasted a while.

?Citi