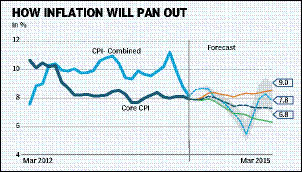

There seems to be wide consensus that RBI will remain on hold at the next monetary policy review meeting on April 1. This view is consistent with the forward guidance in the last policy statement, with CPI inflation having come off over the past couple of months and likely to track (albeit in a bumpy manner) the announced glide path, coming close to the announced way-point of 8% at January 2015 (the accompanying chart shows inflation track in 2014 under different scenarios). However, given the evident central banking antipathy to persisting price pressures, the expectation of core CPI inflation (as well as the core part of the now-low priority WPI inflation) creeping up might induce a surprise pre-emptive hike in rates in the attempt to add another anchor to inflation expectations.

That, however, is not the purpose of this article. Assuming status quo this time, how might the policy rate move in 2014, extending into 2016? Analyst expectations seem divided on rate hikes or cuts in the future, with polls seemingly split equally into ?hold?, ?raise? and ?cut?. Our own thinking is that we might not get a rate cut for the next economic and credit cycle, unless the drivers of inflation become so benign that both the trajectory and expectations suggest a sustained movement down the glide path, to 6% by January 2016.

The problem is that we are currently in a very state-contingent environment, with some clarity likely to emerge only in the next 2 to 3 months. A favourable configuration with a

stable government at the Centre,

normal rains and global recovery will result in outcomes very different from the alternative of a fractured mandate, political uncertainty,

deficient rains and consequent currency and foreign capital flow volatility. Is there a case for a rate cut in either case? The balance of probability seems to suggest not.

In the event of a stable coalition at the Centre, growth supportive measures will be put in place rapidly. Not that growth will move up quickly, probably inching up in the initial year to around 5.5% and then gradually rising to over 7% as capex kicks in. The problem is that will inevitably push up core inflation not just for manufacturing but for many services as well, as corporates, eager to expand beaten-down operating and profit margins, begin to use their improving pricing power (as is already being seen in the Q3 FY14 companies results). With luck, export markets will reinforce this, compressing capacity slacks and enabling price increases. At the same time, if large foreign capital inflows come in?mostly into equities?with markets going up well ahead of earnings improvement visibility, it will invariably impact the real estate market, both due to actual income increases as well as (ephemeral?) wealth effects. Concerns of asset price inflation will add to commodity inflation. If things are as spiffy, why would you need a rate cut? To deliver more credit to productive sectors? Not really. Credit from non-bank sources, both domestic and offshore, would be readily available. High interest rates might actually induce domestic savings, limiting the extent of dependence on foreign funds.

The alternative is the scenario of an adverse outcome. Political uncertainty is likely to lead to significant volatility in capital flows and currency markets, particularly if India?s credit rating is downgraded. The fiscal deficit is likely to be higher than the budgeted 4.1%, inducing an adverse configuration of excess demand. In the doomsday scenario of a failed monsoon, food prices are likely to increase. In this environment, the thinking is likely to be that rate cuts to stimulate growth would be counterproductive. One reason for a cut would be to mitigate the consequences on financial sector asset quality stress, but this might be better dealt with through other forbearance measures.

Straddling both these scenarios, will be the effect of the US yields rising with the steady tapering of the Federal Reserve?s QE, transitioning thereafter, at some point in 2015, into rate increases. In the event of an adverse economic environment in India, the impact is likely to be quite severe?yet another factor reducing chances of policy easing.

In fact, the condition most conducive for a rate cut is a moderate adverse environment with, say, good rains keeping food prices in check and policy indecision resulting in weak project capex revival. In addition, if global commodity prices remain moderate with demand in China not picking up quickly, imported inflation is likely to be restrained.

Ultimately, going back to our starting premise, the decision will boil down to prospects of inflation following the glide path into 2016 and thereafter. With lots of sweat and a bit of luck, we might just about get to the way-points, but the odds are against that, given supply constraints and latent demand.

Abhaysingh Chavan contributed to this piece.

The author is senior vice-president and chief economist, Axis Bank. Views are personal