Guess what the most important voting issue was in the recent general elections (and, indeed, in the four state elections last year)? According to polls, it was not jobs or governance, but inflation!

It is not surprising to see why. For starters, CPI inflation has averaged 9.5% over the last seven years underpinned by stubbornly high food inflation?averaging 11% over that period. The poor?whose incomes are least indexed?also vote in the largest proportions. So high inflation has often directly translated into reduced purchasing power and?in the absence of adequate savings?consumption. It?s no surprise, therefore, that despite a record harvest last year, rural consumption remained weak. Real rural wages had begun to moderate since 2012, in part because nominal wages began to moderate but surging rural inflation has been the real culprit in pulling down real wages.

Second, sustained food inflation in conjunction with the indexation of MGNREGA wages has contributed to a wage-price spiral in the rural economy that has also spilled over into urban wages.

Finally, it is food and fuel inflation that is largely responsible for shaping household inflation expectations. Econometrically, we find that a 100 bps shock to food prices results in a 50 bps impact increase in inflation expectations that decays only over eight quarters! In contrast, a 100 bps shock to core inflation affects expectations by only 30 bps and decays with two quarters. So, taming food inflation is critical to winning the battle on expectations.

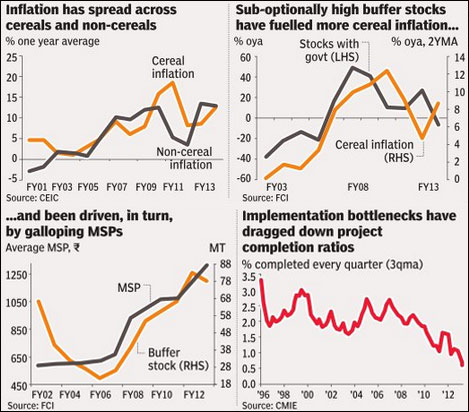

In our view, the government should start by taming cereals inflation. Despite the accumulation of record-buffer stocks over the last two years, cereal inflation has averaged 13%! So, buffer-stocks have clearly lost their ?threat value? in taming expectations. Instead, they have only served to take flow out of the open-market and pressure prices. For starters, therefore, stocks need to be used more effectively and pre-emptively to push down cereals inflation?both by procuring less and releasing more.

But accumulation of cereal stocks is, in turn, a function of the minimum support prices (MSPs) the government offers (see chart). Sharp increases in MSPs in recent years have overly-incentivised farmers to produce rice and wheat, and thereby impeded the supply response to other price signals. So, MSPs have both a direct impact on cereals inflatioan and an indirect impact by inhibiting substitution.

The good news is that, after an average increase of 11% over the last seven years, cereal MSPs increased by only 5% in the last year of UPA II. The new government would do well to limit MSP increases this year and eventually reform it. To its credit, the NDA government showed admirable restraint on the MSP front in its previous stint. The hope and expectation is that this would continue.

But food inflation is not limited to cereals. Non-cereal inflation is even higher at 12% over the last five years with fruits, vegetables and high-protein items becoming particular sources of pressure. A key contributor has been the Agricultural Produce and Marketing Committee (APMC) Act, which has acted as a monopsony at the farm gate, severely restricting agriculture trade, and thereby creating opportunities for hoarding and price manipulation. Removing fruits and vegetables from this mechanism would go a long way in moderating price pressures. But APMC is a state subject, and therefore the central government will have to use significant political capital to lean on states to reform. Prime Minister Modi is well aware of these bottlenecks, and articulated these reforms?and more?in a white paper back in 2011. This article was written before

Tuesday?s food inflation measures and it is heartening to see that the government has already embarked on two of the three aforementioned steps, using buffer stocks efficently and attempting to liberalise fruits and vegetables from the APMC Act.

Jumpstarting capex

Apart from reducing inflation, jumpstarting investments is critical to India?s growth prospects. Quantitatively, we find that of the 695 bps slowdown that India suffered between 2010 and 2013 (ex-agri and community services), almost 30% is because of bottlenecks on the ground and another 15% on account of the associated loss in investor confidence that is closely linked to the ease of doing business. The corollary is that half the slowdown could be reversed if these bottlenecks were completely alleviated and confidence returns. But where should the government start?

We looked at the top 50 projects (in value terms) that are currently stalled. These account for nearly 70% of the total stalled value, and so getting some traction on large projects is crucial. Our search revealed that 55% of stalled projects are because of land acquisition constraints, and another 25% because of issues in the power sector?coal unavailability and state electricity board pricing. Only 8% in this sample were stalled because of environmental clearances?which is understandable given the previous government made significant progress on that front.

So, to the extent that the government can make progress on the land and coal front, they could make a significant dent into implementation bottlenecks. But land acquisition is on the concurrent list and so not under the direct jurisdiction of the central government. Therefore, what the government will likely need to do is both (1) reform the new land acquisition bill to make it more business-friendly; and (2) use political-capital with individual states to ensure that land acquisition issues related to large projects are resolved.

Constraints in the power sector are at both ends of the spectrum?the unavailability of domestic coal (forcing the import of coal which is currently 20-25% more expensive) and the inability to sell to SEBs that are cash strapped. The latter is a more complex problem that requires meaningful tariff hikes, is under the domain of the states, and is politically very sensitive. For starters, therefore, we recommend the government prioritise coal production in India. India has among the largest coal reserves in the world and yet it is the fourth-largest importer of coal because CoaI India?s production has literally ground to a halt.

So what could the government do? For starters, building three new rail-lines covering about 200 km (though logistically not trivial given the terrain) potentially opens up another 200 million tones of coal per annum that can be mined and transported from Chhattisgarh, Orissa and Jharkhand. This needs to be complemented by injecting private efficiencies into Coal India. One option is reform by stealth. Future coal licences should be allocated to the private sector, who would be able to extract coal more efficiently and sell it to Coal India who, in turn, could on-sell it to power producers.

Bottom line: If the government can begin to tackle coal and land in the first year, the capex cycle could finally get going.

(This is the first of a two-part series)

Co-authored with Toshi Jain, JP Morgan Chinoy is chief India economist, JP Morgan