Drawing from a wider mandate, monetary policy in India has evolved to have multiple objectives of price stability, financial stability and growth. These objectives are not inherently contradictory, rather mutually reinforcing. The Reserve Bank?s approach recognises that price and financial stability are important for sustaining high levels of growth which is the ultimate objective of public policy. The Reserve Bank?s approach to financial stability has been proactive and preventive rather than reactive. Its role as monetary policy authority, well integrated with macroprudential regulation and microprudential supervision, with an implicit mandate for systemic oversight has enabled the Reserve Bank to exploit the synergies across various dimensions.

Even before the crisis, the institutional arrangement in the financial sector was already in place for inter-regulatory co-ordination to monitor financial stability in the economy. A High Level Co-ordination Committee on Financial Markets (HLCCFM) was set up in 1992 with the Governor of the Reserve Bank as Chairman, and the Chiefs of the Securities and Exchange Board of India (Sebi), the Insurance Regulatory and Development Authority (Irda) and the Pension Fund Regulatory and Development Authority (PFRDA), and the Finance Secretary to Government of India as members. However, post-crisis, the collegial approach to financial stability has been further strengthened by constituting the Financial Stability and Development Council (FSDC).

Even before the crisis, the institutional arrangement in the financial sector was already in place for inter-regulatory co-ordination to monitor financial stability in the economy. A High Level Co-ordination Committee on Financial Markets (HLCCFM) was set up in 1992 with the Governor of the Reserve Bank as Chairman, and the Chiefs of the Securities and Exchange Board of India (Sebi), the Insurance Regulatory and Development Authority (Irda) and the Pension Fund Regulatory and Development Authority (PFRDA), and the Finance Secretary to Government of India as members. However, post-crisis, the collegial approach to financial stability has been further strengthened by constituting the Financial Stability and Development Council (FSDC).

In my opinion, the global financial crisis has fundamentally altered the way we used to view monetary policy and financial stability and the interface between them. However, there are issues which entail further work in three key areas. First, a relook at monetary policy framework in terms of both objectives and instruments towards a clear recognition of financial stability. Second, to put in place an appropriate institutional mechanism drawing upon countries? own experience and history for better co-ordination among the concerned regulatory entities to deliver on financial stability. Third, address the communication challenge of multiple objectives to preserve central bank credibility to ensure price and financial stability. Let me now elaborate on each of these three aspects.

(i) Monetary policy framework

The view that monetary policy framework should allow policymakers to lean against the build-up of financial imbalances, even if near-term inflation expectations remain anchored, is gaining importance. While there is little doubt that monetary policy framework of central banks needs to change, the moot point is what should be the ideal monetary policy framework for better analysis of the macroeconomic effects of financial imbalances? One approach could be to formally broaden the set of information variables for monetary policy decision making: in a way, for example, the two pillar approach of the ECB or the multiple indicators approach of the Reserve Bank of India that factors in financial considerations into monetary policy. The multiple indicators approach has the advantages of broad-basing monetary policy operations on a large set of information such as money, credit, asset prices, interest rates and exchange rate and providing flexibility in the conduct of monetary management. Such approach, however, may involve a greater element of judgment.

At an operational level, the most widely accepted presentation of monetary policy reaction function that combines both inflation and growth objectives is the ?Taylor Rule?. The Taylor rule can be augmented by adding financial variables to the standard monetary reaction function based on inflation and the output gap so as to enhance central banks? ability to react to financial stability concerns. However, efficiency of such a formulation needs to be tested. Whichever framework is adopted, there should be flexibility for the central bank to respond to potential imbalances and the risks, apart from growth and inflation control.

(ii) Institutional design for better coordination

The recent crisis and the subsequent response have shed new light on the critical role of central banks in promoting financial stability. However, it needs to be recognised that this added responsibility should not come at the cost of their conventional role for price stability. This is more relevant particularly for central banks in EMEs which admittedly, are yet to achieve that level of credibility as their advanced economy counterparts. For many EMEs, exchange rate stability is an important objective, and without price stability it is not possible to maintain exchange rate stability. Furthermore, the financial markets and institutions have grown in complexity, the oversight and regulation of which could be beyond a single entity such as the central bank. Hence, financial stability would have to be a joint responsibility, though the central bank could have a dominant role by virtue of it being the natural lender of last resort.

The challenge for a central bank is to achieve multiple objectives without losing credibility as a monetary authority solely responsible for price stability. This would be possible only if policies implemented by various stakeholders in financial stability are coherent.

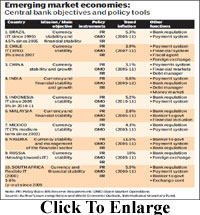

The design of co-ordination mechanism may, however, vary across countries depending on the nature and size of their financial systems and their own historical experience. In fact, efforts towards greater institutionalisation of co-ordination mechanism have already begun. Most prominent examples are the newly created bodies, both in advanced countries and EMEs, like the Financial Stability Oversight Council in the US, the Financial Policy Committee (Interim) in the UK, the European Systemic Risk Board for the European Union, Financial Regulation and Systemic Risk Council in France, Financial Stability Council in Chile, Council for the Stability of the Financial System in Mexico and Financial Stability and Development Council in India. In some other countries, financial stability framework has been strengthened by setting up committees in central banks to gauge systemic risk (e.g., Brazil in 2011).

(iii) Central bank communication

In a market-determined system, central banks have placed a greater reliance on transparency and communication to enhance monetary policy transmission and establish accountability to the public for their decision-making. So far the experience shows that communication on monetary policy issues has moved from complete secrecy, to constructive ambiguity to transparency. For instance, the Fed and the ECB have in recent years frequently provided fairly direct indications about future interest-rate decisions in their official statements. We, in the RBI, have also started giving forward guidance since September 2010. However, there are several challenges.

It is not easy to communicate clearly on a single objective. Going forward, as central banks broaden their mandates and institutional design grows in complexity, so also will the communication challenges. For example, if a central bank were to ease monetary policy on financial stability concerns even when inflation is high, it risks unhinging of inflation expectations, which in turn could complicate financial stability.

We, in the RBI, had to face communication challenge when we reduced cash reserve ratio (CRR) of banks in January and March 2012 on liquidity concerns even when inflation was above our tolerance level. While some interpreted it as premature reversal of tight monetary policy stance, others saw this as a pure liquidity action not inconsistent with our monetary stance.

If the policy measures are not properly guided and not understood as intended, they may not transmit the right signal and eventually prove to be a noise to financial market entities. Guidance by central banks, at best, could be conditional because of the provisional nature of immediate available information set, limitations of macro models, incomplete knowledge and uncertainties about the evolution of the economy and periodic unanticipated shocks. Thus, transparency in communication is a double-edged sword which at times could produce unintended consequences. As central banks broaden their objectives so also they have to hone their communication skills.

Extracted from a speech made by the author, executive director, Reserve Bank of India, at the 2012 Central Bank of Nigeria Board Retreat, Cape Town, South Africa, titled ?Price Stability and Financial Stability: An Emerging Market Perspective?