Even as the NDA government is believed to be contemplating an increase in the cap for foreign direct investment (FDI) in insurance to 49% from 26%, private sector life insurers are struggling to make ends meet. A higher FDI ceiling would allow for more capital infusion by foreign players and pave the way for many companies to raise funds from the capital market through initial public offerings (IPOs).

However, if the voting rights of promoters are frozen at 26%, as some reports suggest the government may be inclined to do, foreign players may be reluctant to invest further.

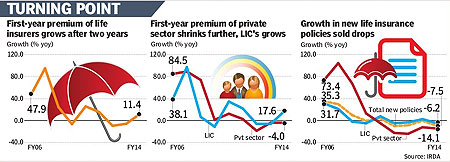

The last few years have been exceptionally difficult for the industry, with new business premiums for the life insurance space coming off by 25% from the highs of 2011 due to a very challenging regulatory environment as also a sluggish economy. While high inflation prompted households to park their savings in physical rather than financial assets, instability on the regulatory front made it difficult for insurers to sell products.

On the contrary, they were compelled to redesign products and incur additional costs to reintroduce and sell them. Due to the change in regulations in October 2010, the share of unit-linked products, which accounted for 80% of private sector players? business five years back, has fallen drastically. However, the turnaround in the stock market, experts point out, could see these products becoming popular once again. Currently, however, traditional products are more in demand although the industry is grappling with the new norms put in place by the Insurance Regulatory and Development Authority (Irda) in January 2014.

With the incentive structure for agents made less attractive ? as in case of mutual funds ? insurers have faced challenges on the distribution front, too. The existing commission structure for channels is one of the lowest in the world, making it less attractive for intermediaries to sell life insurance.

According to one estimate, for the top seven private sector players, agency sales account for less than 40% of total sales.

With agents disincentivised, insurers depended more on the bancassurance channel, but that too hasn?t delivered the kind of growth it promised. As experts point out, insurance remains a ?push product? for which intermediaries need to be encouraged. While there is a move to let banks become brokers, banks have been reluctant to play that role.

For their part, insurers would need to cut costs; while the opex-to-total premium ratio has improved from approximately 40% in 2004 to 18% ? according to an estimate by consultancy Boston Consulting Group in 2013 ? the ratio needs to be brought down to 7-8 % over time.