Shall we read between the lines? We believe credit costs are likely to stay high in the medium term as operating performance is weak and leverage remains high. Our belief is based on our analysis of companies (20% of CDR cases by loan-size) that restructured their loans through CDR (corporate debt restructuring). Our extended study of select companies shows different approach to debt repayment, which makes prediction of loan impairment for the large corporate segment extremely challenging.

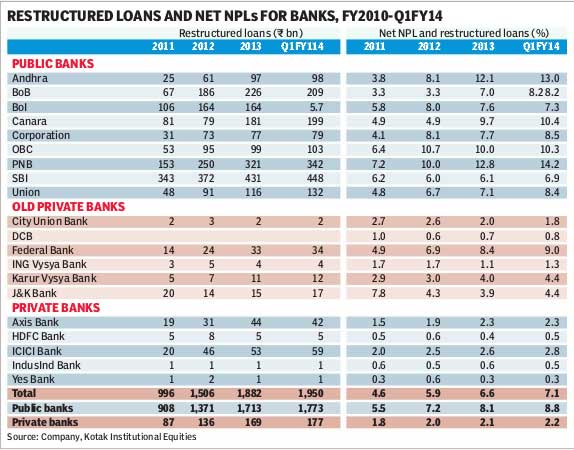

Companies in the CDR forum are struggling: FY13 was another challenging year for companies that restructured loans through the CDR forum. Our analysis of companies (25 companies with debt of R465 bn, about 20% of the debt referred to the CDR) reiterates our view that slippages and credit costs are unlikely to soften?(i) leverage has deteriorated with loans increasing 8% year-on-year, especially long-term loans, which increased 15% y-o-y; (ii) operating performance has been weak with sales declining 7% y-o-y, compression of Ebitda margin (13% in FY2013 against 17% in FY2012), a 6x increase in losses and a decline of 66% y-o-y of cash from operations; (iii) restructuring of loans eased the repayment cycle for companies, resulting in a decline in payment in the near term (13% of loans in FY13 against 17% in FY12).

Predicting corporate slippages is tough: The link between the economic slowdown and corporate loan impairment has been weaker than we expected. Companies, unlike SME or retail borrowers, probably have access to alternative sources of credit cushioning against a sharp rise in NPLs (non-performing loans) despite a substantial deterioration in cash flow and/or debt servicing ability. While we discuss many methods we leave open to interpretation the implications of such transaction, and whether unavailability of these options could have resulted in substantially higher defaults than those printed so far.

However, we lay a few disclaimers?(i) we are not sure if some of these companies have been classified as defaulters or the companies are accessing credit where sanctions were made substantially prior to the current state of affairs and banks are obliged to fulfill their commitments and (ii) we believe the transactions analysed are indicative and not exhaustive in nature.

Highlights from annual reports: Our analysis of select transactions from the balance sheet indicates companies have been able to repay debt by a combination of (i) conversion of rupee debt to foreign currency debt with extended periods of repayment; (ii) new lines of credit offered by other banks; (iii) refinancing of loans, especially when assets are operationalised; (iv) lending at various levels in the company and allowing companies to place money with their subsidiaries through inter-corporate deposits; (v) early conversion of collateral and (vi) unsecured/general purpose loans.

Real estate?banks have increased exposure despite defaults: Despite a challenging business environment for real estate companies and delay in repayment/default to non-bank financial institutions, we have broadly seen that repayments have been quite regular.

Nevertheless, we are quite surprised that many of these companies continue to receive fresh lines of credit.

?Kotak Institutional Equities